The vast majority of retirees need to stay of their properties and age in position so long as conceivable. Certainly, many of the monetary plans for my retired shoppers venture them to stick of their house, or a house of identical worth, for his or her complete lives.

That makes very best sense when you plan on leaving your paid-off house in your beneficiaries upon your dying.

However, for lots of retirees, an absolutely paid-off house represents untapped fairness that may result in underspending all through retirement, or no less than a major relief in way of life as they age.

The answer is to imagine a house fairness unencumber technique – a time period I first heard closing month when Dr. Preet Banerjee wrote about biases round space wealthy, money deficient householders.

Under are the seven other house fairness unencumber schemes that had been indexed:

- Opposite mortgages

- House Fairness Traces of Credit score (HELOCs)

- 2d mortgages

- Refinancing

- Promoting to downsize right into a smaller owned house

- Promoting to transport right into a apartment house

- Promoting to lease-back the similar house

Unlocking all or a portion of your own home fairness can considerably toughen your retirement result, and but many retirees aren’t even making an allowance for their very own house fairness unencumber technique as a part of their retirement plan.

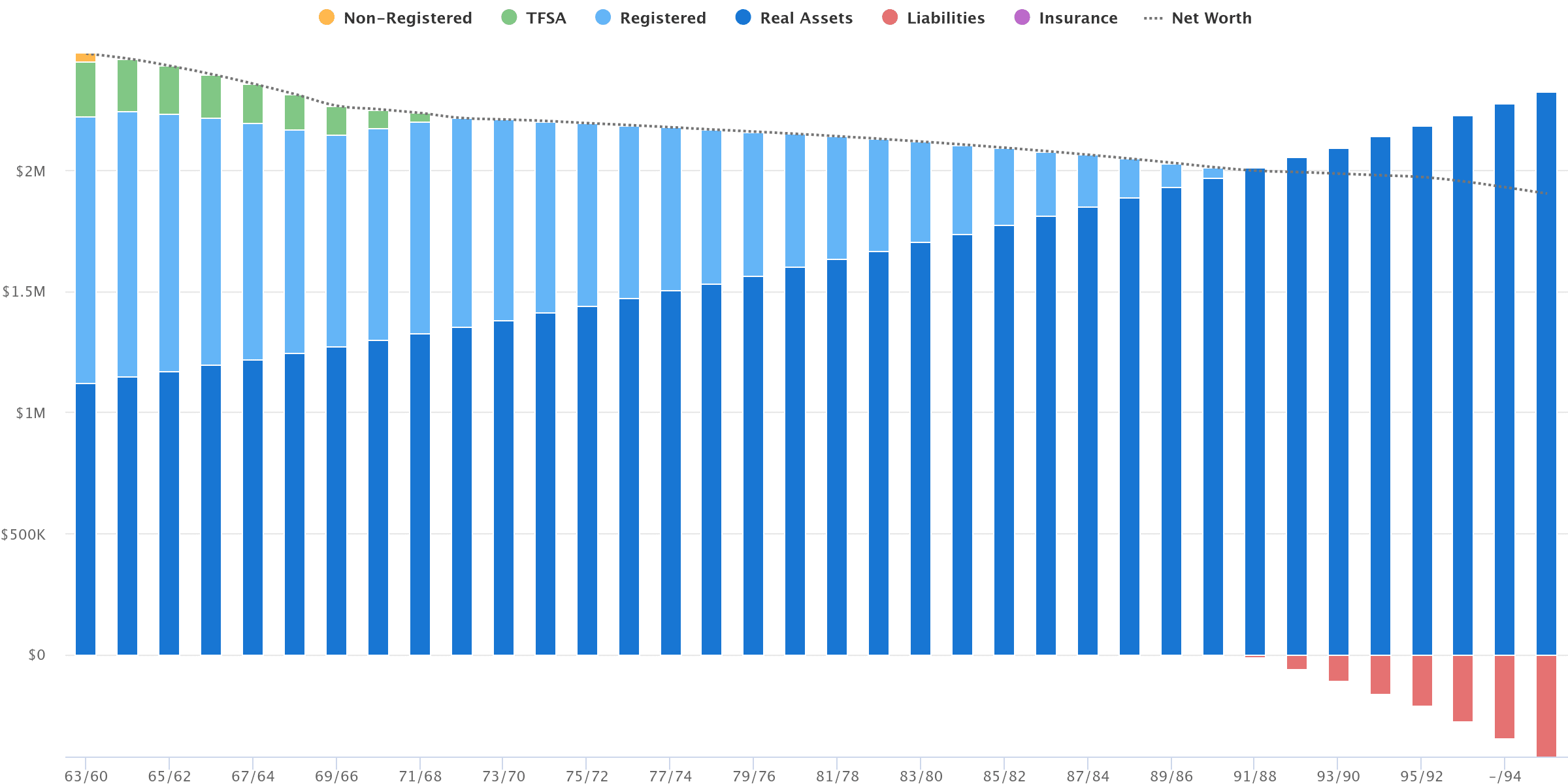

Under I’m going to percentage an instance of a up to date retired couple, Joe and Linda Davola, who reside in Ontario and retired on the finish of closing yr at ages 63 and 60, respectively.

They’ve mixed property of $1.4M stored throughout their RRSPs, TFSAs, non-registered financial savings, and Joe’s LIRA. They actually have a paid-off house value $1.1M for a complete web value of $2.5M.

Joe and Linda want to spend $100,000 according to yr after-taxes all through retirement. They paintings with an advice-only monetary planner to look what’s conceivable.

The planner runs a projection that presentations after-tax spending of $100,000 according to yr, emerging with inflation at 2.1% once a year till Joe’s age 75 yr, after which expanding via simply 1.1% once a year till Joe’s age 95 yr.

On this state of affairs, Joe and Linda stay of their paid-off house and don’t contact the fairness. Sadly, they run out of cash in Joe’s age 91 yr.

Along with this not up to very best result, the planner additionally issues out that lifestyles doesn’t all the time transfer in a instantly line. In reality, they are going to maximum for sure incur one-time prices similar to house renovations, car substitute, bucket listing shuttle, or monetary presents to their kids or grandchildren all through retirement.

The planner meets with Joe and Linda and in combination they get a hold of a listing of those one-time bills that may or might happen over the following 5-10 years.

- Bucket listing commute to New Zealand in 2025 – $20,000

- Kitchen renovation in 2026 – $40,000

- Finance a brand new car from 2027 to 2030 – $12,000 according to yr

- Improve HVAC in 2031 and 2032 – $7,500 according to yr

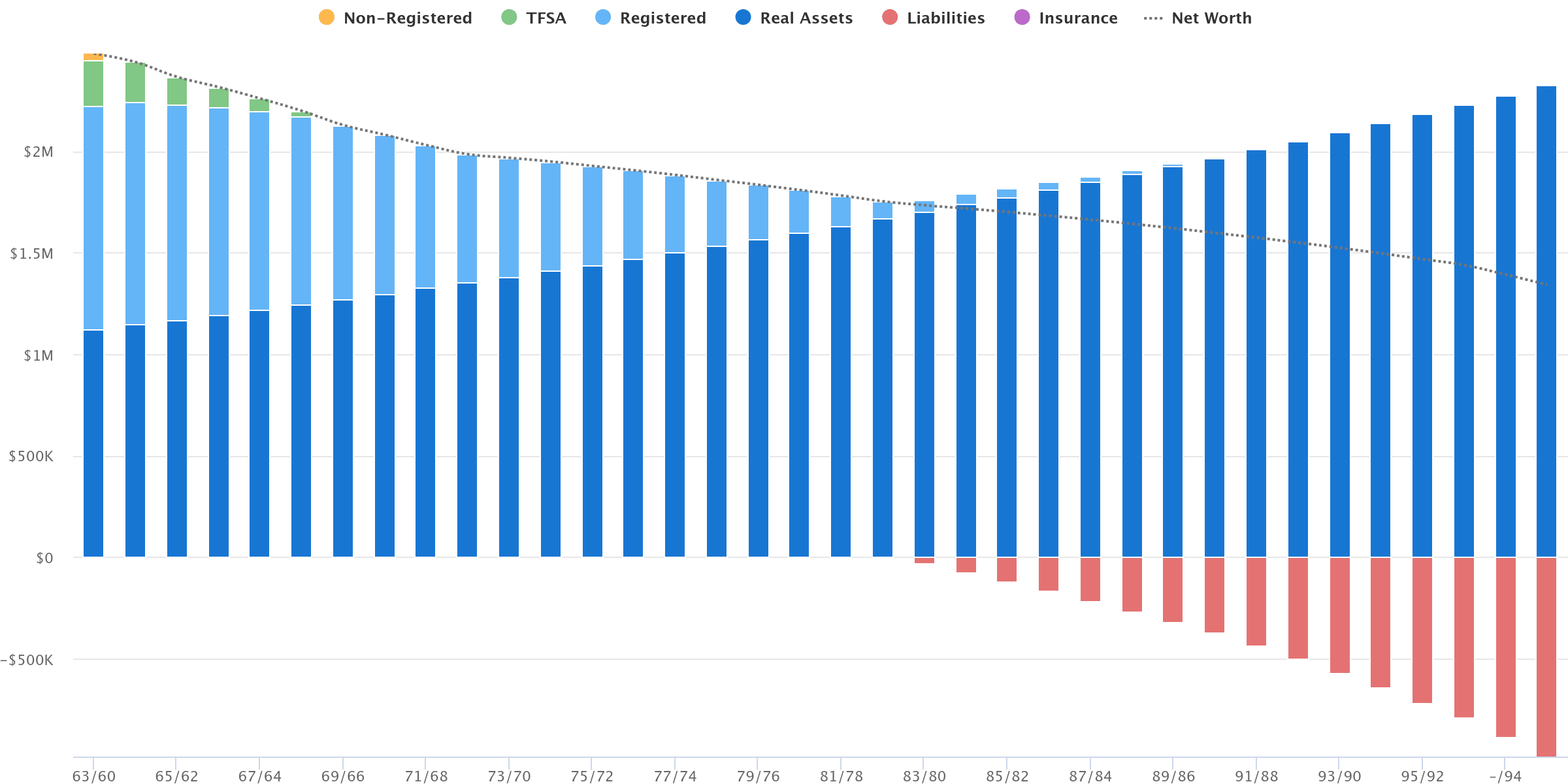

Once we upload the one-time bills into the plan, and stay spending consistent at $100,000 according to yr, the result will get considerably worse. Now the Davolas run out of cash at ages 83 and 80, respectively. That’s 8 years previous than anticipated.

At this level it turns into crystal transparent that in an effort to care for their desired way of life the Davolas will want a house fairness unencumber technique.

They debate promoting the home and renting, however Linda likes the reassurance that incorporates house possession and worries about emerging apartment prices and the specter of having to transport once more.

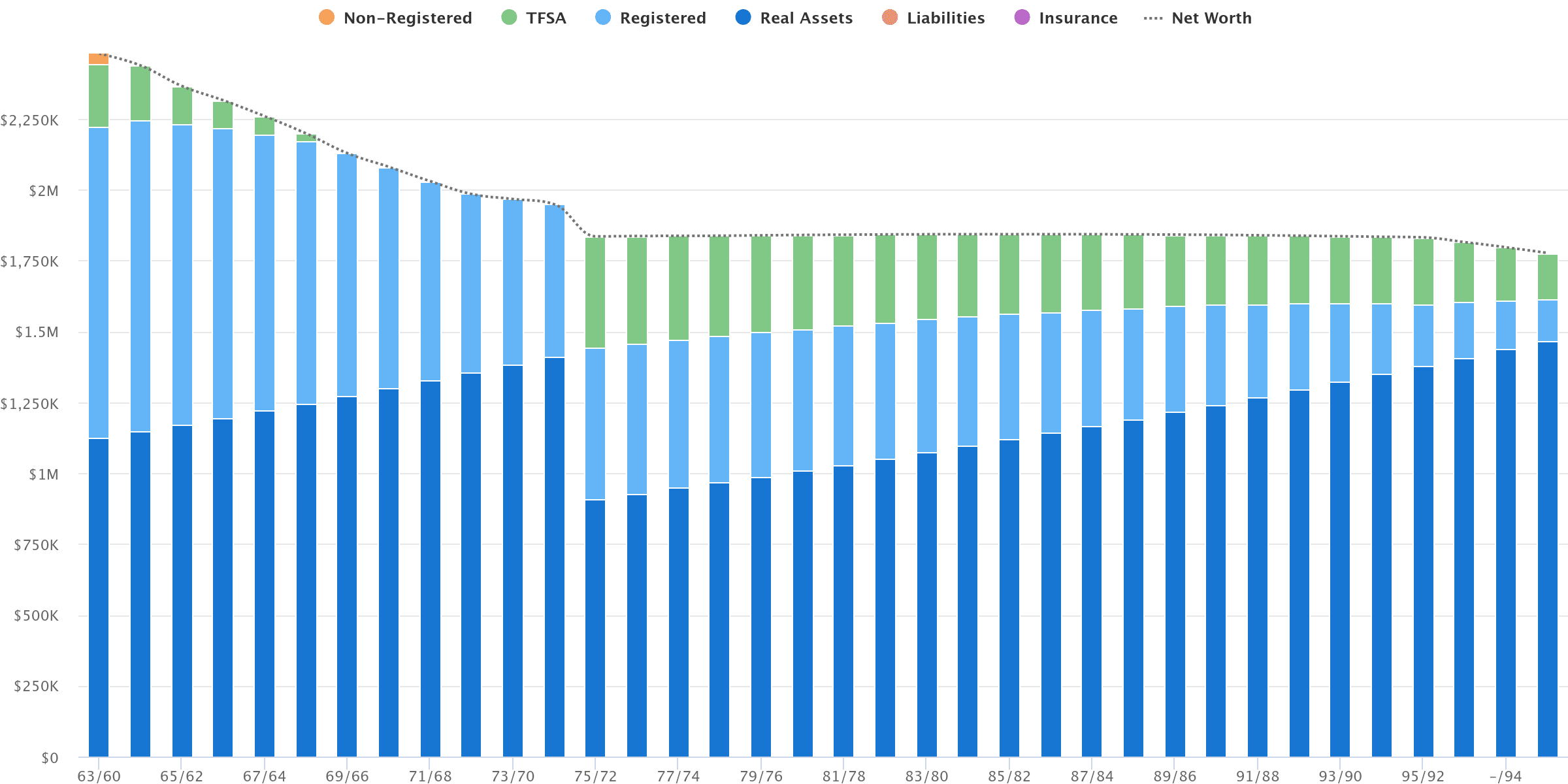

House Fairness Free up Technique

The Davolas make a decision the most productive plan of action can be to downsize to a rental in 12 years (Joe’s age 75 yr). They’d promote their house for $1.4M and purchase a rental for $900,000* – unlocking part one million bucks in house fairness that can be utilized to care for their way of life.

*That $900,000 rental bought in 12 years is the identical of buying a $700,000 rental lately.

Their planner runs the numbers and means that no longer solely can they proceed spending $100,000 till age 95, however they may be able to additionally give an early inheritance of $50,000 each and every to their two kids from the proceeds in their space sale.

Right here’s what it looks as if:

Via “liberating” $500,000 of untapped house fairness, the Davolas can refill their TFSAs and provides an early inheritance reward to their kids.

They are able to care for their desired way of life till age 95, and nonetheless go away an property to their two kids value $1.73M. That’s in long term bucks, thoughts you, so it could be like leaving an property value $835,000 lately – or the rental plus $135,000 in financial savings.

Ultimate ideas

The need to stay in your house so long as humanly conceivable and keep away from long-term care makes very best sense. However lifestyles doesn’t all the time end up as deliberate, and it’s smart to keep away from making choices when our choices and psychological capability could also be restricted.

That’s why it’s sensible to imagine your own home fairness unencumber technique in advance originally of retirement.

Are you able to truthfully see your self ultimate on your circle of relatives house into your 80s and 90s?

We additionally have a tendency to vastly overestimate our skill to undergo important spending cuts. I listen at all times from retirees who suppose they’ll simply lower $20,000 according to yr or extra from their spending at 75 or 80.

In truth, the decline in spending from the “go-go” years to “slow-go” years to “no-go” years is a lot more refined. Like, as a substitute of spending proceeding to upward push with inflation it rises via inflation minus 1% on your slow-go years, after which merely stays flat on your no-go years.

So, as a substitute of depending on a drastic relief in way of life spending (deficient long term you!), imagine how the use of all or a portion of your own home fairness can are compatible into your retirement plan and mean you can care for the usual of residing that you simply’d love to experience.

And, for my lifelong renters, it’s true that you simply gained’t have the margin of protection and choices that house homeowners have in retirement, however I’d additionally argue that when you’ve prudently stored and invested the (ceaselessly important) distinction between renting and residential possession, you’re already on target to maximise your spending all through retirement with out leaving any untapped house fairness at the desk.