After I first create a monetary plan for a shopper I inform them that that is my preliminary interpretation in their present state of affairs and long term objectives mapped out over the years. It’s a projection or street map according to their present trajectory.

I’m in search of clues, patterns, purple flags, and alternatives. The numbers are telling a tale about what’s conceivable.

Right here’s what I imply.

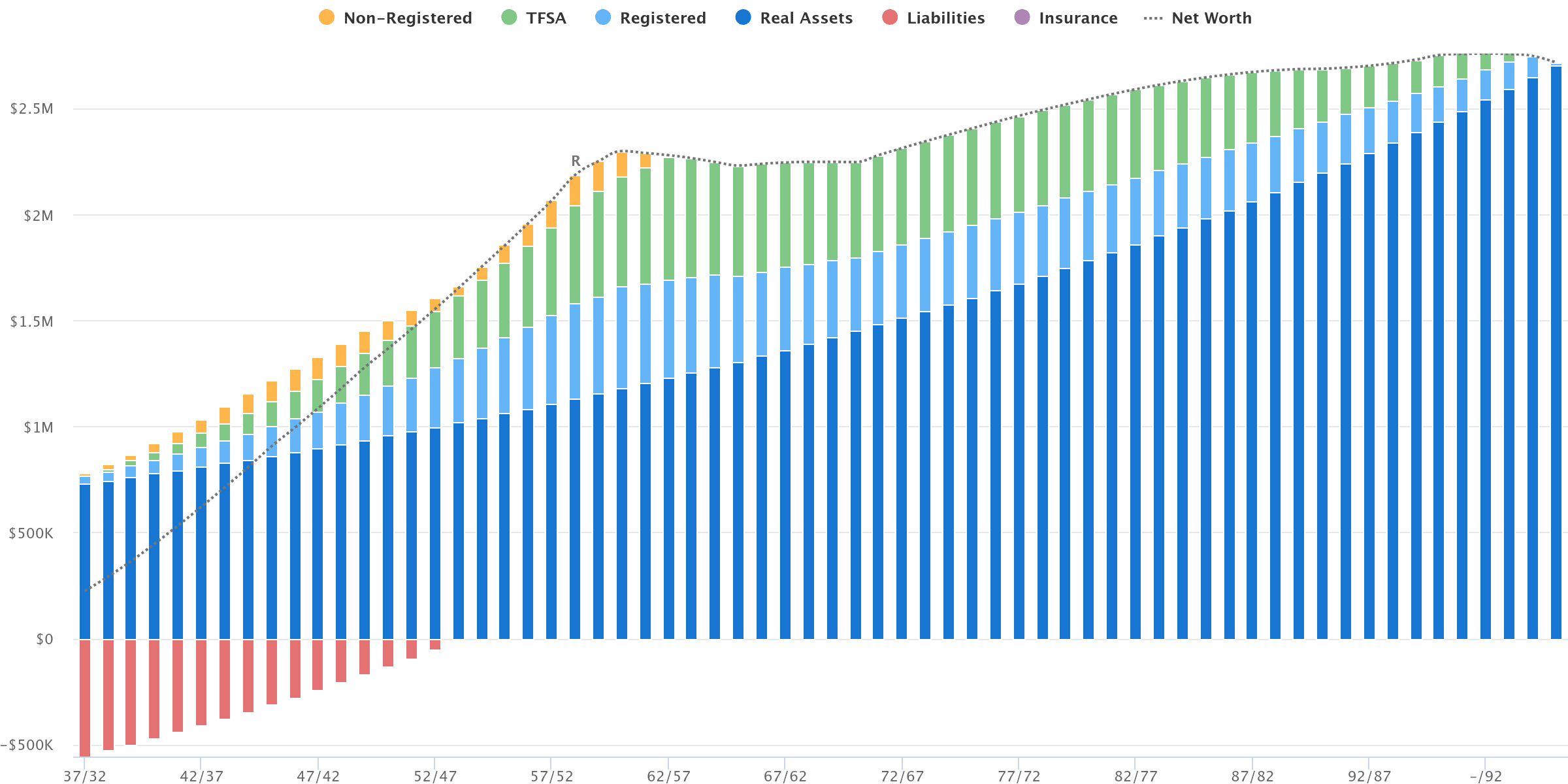

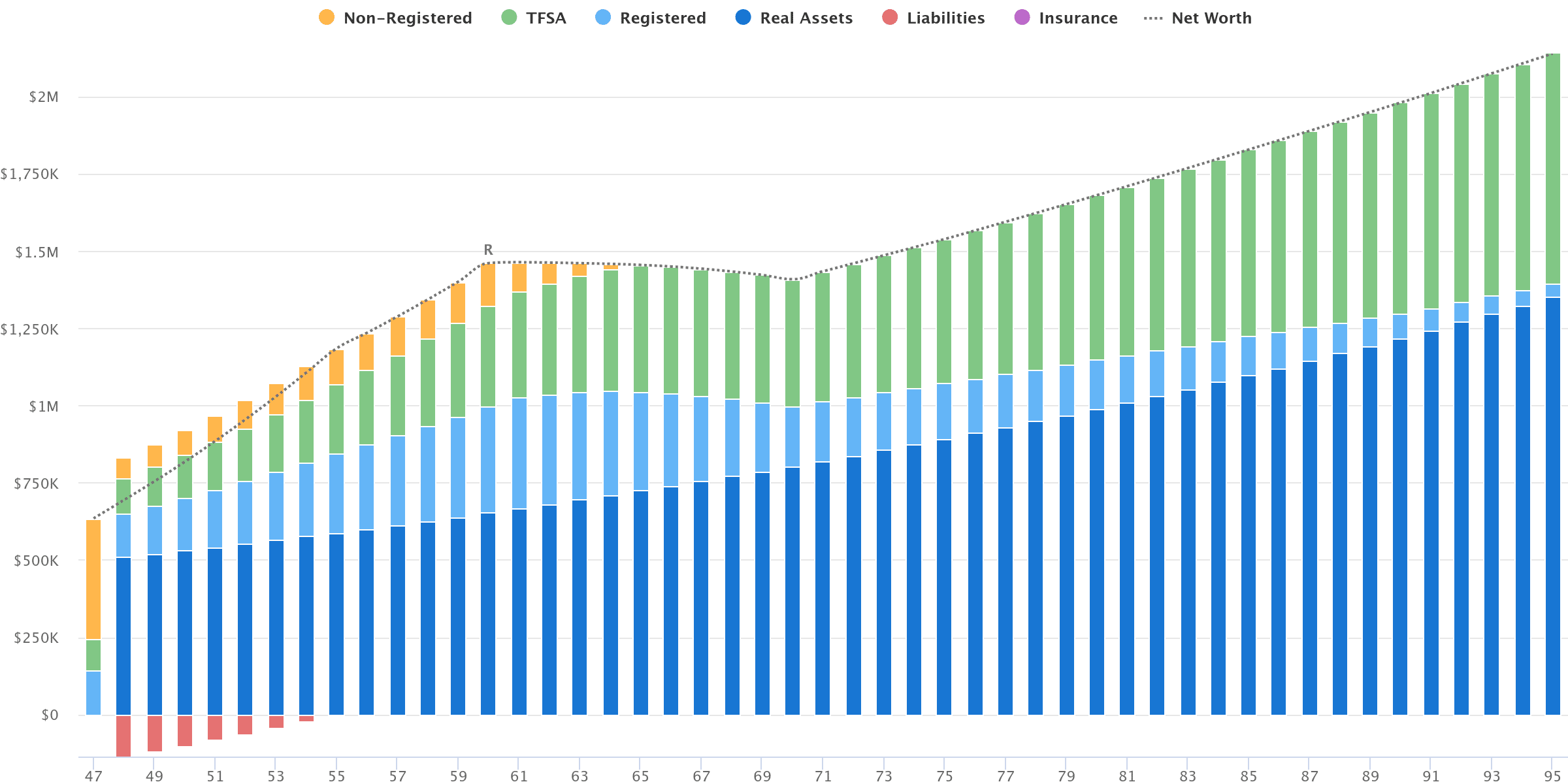

A normal internet value projection right through your running years is going up and to the appropriate. That is sensible, as you earn source of revenue, give a contribution in your financial savings, get a fee of go back in your investments, and pay down debt.

However running households even have competing monetary priorities. Source of revenue interruption from parental go away, kid care, automobile bills, house renovations, even upsizing a house are all actual probabilities that younger households are coping with.

Your own home is your greatest asset and also you’re deep in loan debt. You could have little in the way in which of financial savings and really feel such as you’re now not making any growth when you’re coping with one-time, brief prices. However zooming out you’ll see a mild on the finish of the tunnel.

Kid care prices subside, source of revenue will increase, and loan bills not really feel like they’re taking over your entire disposable source of revenue. You get started making some significant growth in your retirement financial savings objectives and your internet value heads up and to the appropriate.

As soon as the loan is paid off, you will have choices to ramp up financial savings or even contemplate early retirement.

At this level I’m in search of clues as as to whether you’re on track to retire early, or if you happen to’d want to downsize your house to make sure you’ll handle your way of life all the way through retirement, or if you’ll find the money for to extend taking CPP and OAS to protected extra lifetime source of revenue.

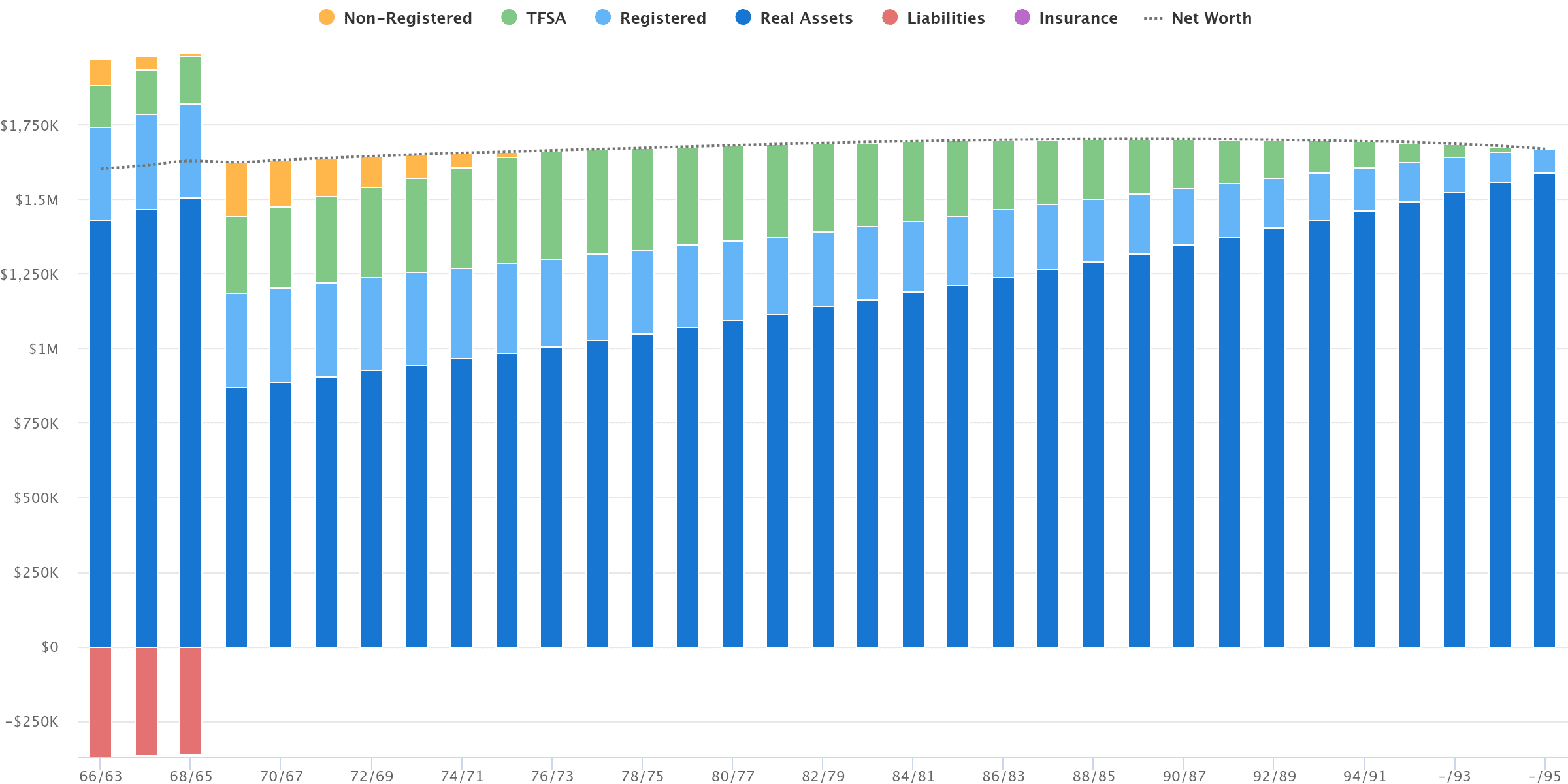

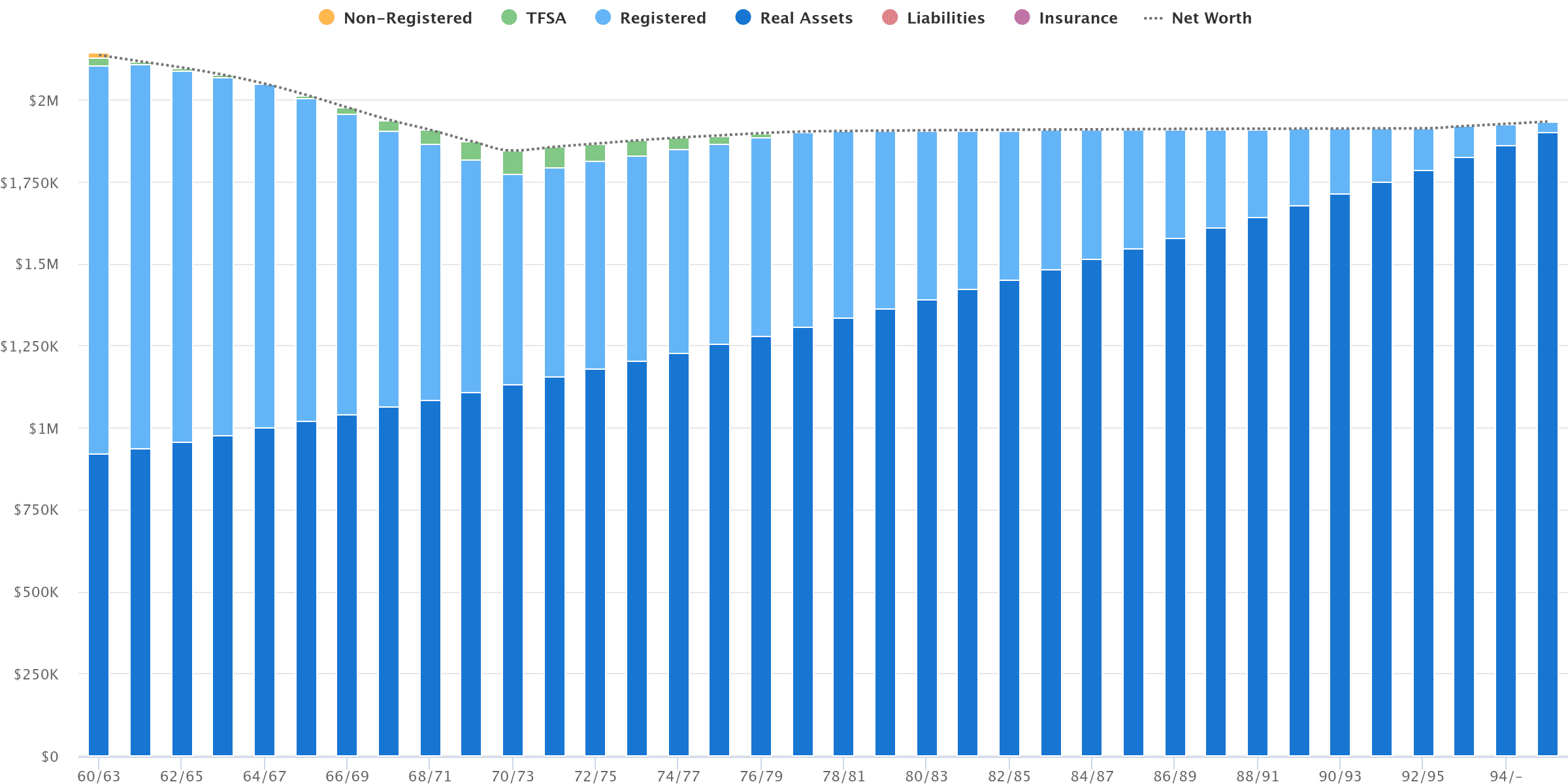

I latterly wrote a few idea known as your house fairness unlock technique and it’s turning into increasingly vital to consider, particularly in excessive price of residing spaces the place retirees is also sitting on untapped house fairness of $1M to $2M (or extra).

Within the above instance, the retired couple downsize their house at or in a while after retirement to get rid of their loan, upload valuable house fairness again into their financial savings, and make sure they are able to handle their way of life all the way through retirement.

There’s nonetheless a slight risk of operating out of cash of their outdated age, however they do have the paid off house fairness of their downsized house to fall again on, simply in case.

An alternative choice is to promote the circle of relatives house and hire all the way through retirement. This has the additional advantage of having the ability to maximize retirement spending, however with the trade-off of now not having a fall again way to promote the house in case of unplanned spending shocks or deficient marketplace returns. A prudent spending plan is paramount on this case.

What about singles? In my enjoy, singles may have a troublesome time in two stages of lifestyles.

One, purchasing a area as a unmarried in a excessive price of residing house is also extremely difficult.

Two, with out the advantage of a spouse with whom to separate source of revenue in retirement, singles face upper tax charges and are much more likely to incur Outdated Age Safety clawbacks.

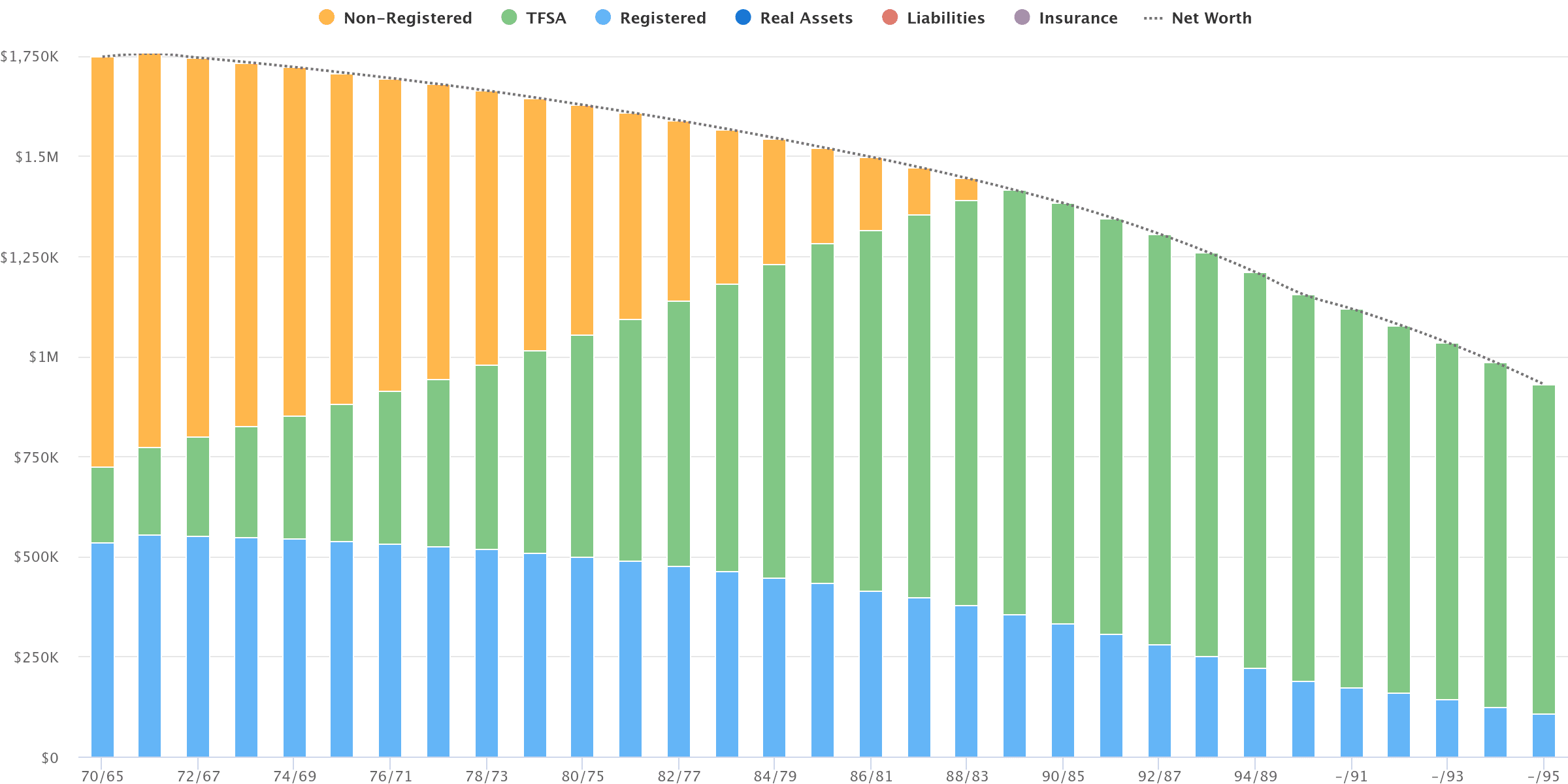

Within the above state of affairs, this unmarried person was once lucky to obtain a small inheritance in her late-40s to in any case have the ability to find the money for a rental in her desired location and worth vary.

If she assists in keeping her spending in line with the way of life she loved in her ultimate running years then it’s conceivable that she received’t need to promote that rental to fund her long-term retirement spending. However, in lots of instances, singles who purchase a house are much more likely to need to downsize or promote their house to handle their way of life.

In any case, a number of of my shoppers have an interest within the “die with 0” solution to retirement making plans. I don’t adore it, as a result of spending each greenback and having your closing cheque jump leaves no margin of protection for unplanned spending shocks.

So, for householders taking a look to maximise spending, I want to turn them a “die with 0, however keep in your home” state of affairs. This fashion, you will have a fall again way to promote your house and transfer right into a retirement facility if important as you run out of cash.

Your numbers inform a tale about what’s conceivable. Projected over the years, we will be able to begin to see patterns, purple flags, and alternatives on your monetary plan. We’re in search of clues to look if you happen to’re on track or want to trade route.

I’ll be truthful, extra continuously than now not those internet value projections display that my shoppers can spend greater than what their present finances suggests.

However, continuously we do see purple flags that recommend shoppers will want to make tricky alternatives about running longer, downsizing or promoting the house, or decreasing spending to make sure they received’t run out of cash.

Wish to know what sort of tale your numbers inform? Achieve out to me and we’ll get a hold of a monetary plan.

This Week’s Recap:

Have you thought about your house fairness unlock technique?

How a lot do you intend to spend in retirement?

Right here’s how I plan to catch-up on my TFSA room.

Promo of the Week:

We activated participant two for our rewards playing cards technique, which means previous this yr I signed up for the American Specific Industry Gold card, hit the minimal spend goal to achieve the welcome bonus, after which referred my spouse (participant two) to get the similar card in her title.

The result’s 15,000 further Club Rewards issues for me for the referral, and now my spouse has an opportunity to earn 75,000 Club Rewards issues after spending $5,000 within the first 3 months.

We activated participant two for our rewards playing cards technique, which means previous this yr I signed up for the American Specific Industry Gold card, hit the minimal spend goal to achieve the welcome bonus, after which referred my spouse (participant two) to get the similar card in her title.

The result’s 15,000 further Club Rewards issues for me for the referral, and now my spouse has an opportunity to earn 75,000 Club Rewards issues after spending $5,000 within the first 3 months.

Weekend Studying:

Will have to I pay myself dividends from my corporate to steer clear of CPP premiums?

Many Canadians personal overseas assets. Whether or not its shares, ETFs, bonds, actual property, and even crypto, you will have some tax duties to believe.

Non-public credit score finances are pitched as secure and strong, however buyers aren’t getting the rest particular for the excessive possibility and charges.

Is $1 million in financial savings sufficient to retire on if we withdraw 4% according to yr?

An out of this world dialog with the Canadian Sofa Potato Dan Bortolotti at the Rational Reminder podcast closing week:

A Wealth of Commonplace Sense blogger Ben Carlson asks how would you make investments $14 million?

RRSP to RRIF, and LIRA to LIF: Right here’s the way it all will get performed.

How Wealthsimple is making an attempt to overcome the massive banks at their very own loan recreation:

“I’ve noticed loan cashback gimmicks up to now, however this one is extra fascinating. Not like different lenders’ rebate provides, Wealthsimple’s calculator makes it simple to estimate the financial savings — and they have got compelling financial savings choices.”

Right here’s why variable fee mortgages are the most productive guess to prevent cash after Financial institution of Canada minimize.

Dr. Preet Banerjee explains why AI outperforms people in monetary research, however its true worth lies in bettering investor behaviour.

Andrew Hallam stocks the unexpected reality: kids most probably build up your wealth.

Anita Bruinsma explains why divorcing oldsters are dealing with tricky alternatives amid sky-high actual property costs.

The only position in airports other folks if truth be told need to be: Throughout the festival to trap prosperous vacationers with sumptuous lounges.

In any case, Nick Maggiulli appears to be like at when maximizing bank card rewards is worthwhile and when it isn’t.

Have a really perfect weekend, everybody!